Mr. Crapo (00:00):

… directly to consumers through health savings accounts, which are now available on the Obamacare exchanges because of a provision in the One Big Beautiful Bill. Leveraging long-standing provisions in the tax code, like the medical expense deduction, could help patients further defray high out-of-pocket costs. To guide future policymaking, a commission at the CMS could evaluate and recommend options to further reduce costs for all Americans. We should fund cost- sharing reduction subsidies, which mitigate out-of-pocket costs for low-income enrollees, reduce premiums for all Obamacare plans by over 10% and save taxpayers money.

(00:44)

We should also enact PBM reform, which would realign incentives in the drug supply chain to lower patient costs at the pharmacy counter. Ranking Member Wyden and I intend to reintroduce the Senate Finance Committee's package, which we negotiated in the last Congress on a bipartisan basis, and we are going to do that shortly. We invite all members of this committee to join us as co-sponsors as we move this bill to the President's desk, hopefully soon, for his signature.

(01:13)

The PBM process undertaken by this committee should serve as a model for other reforms. Healthcare integration can produce efficiencies, but too much consolidation can result in monopolistic powerhouses that block innovative disruptors, limit market competition and constrain consumer choice. We must also seek to expand care access points to avoid costly treatment delays. Establishing long-term telehealth flexibility would allow patients to receive care in lower-cost settings.

(01:49)

We should reform our clinician payment system to bolster the workforce, increase the reimbursement stability for independent practitioners, and allow a wider variety of providers to deliver services. Swift coverage of cutting-edge innovations and emphasis on preventive measures can reduce higher long-term costs. We cannot transform our broken healthcare system overnight, but this committee has a proven record of bipartisan success and today's hearing is the first step in building the foundation for this reform. I again thank our witnesses and I now turn to Ranking Member Wyden for his opening remarks.

Mr. Wyden (02:30):

Thank you very much, Mr. Chairman. Today, we discuss the healthcare crisis facing American families. At this very moment, millions are logging on to healthcare.gov and seeing premiums double, triple, or in the case of our guests from Oregon, even worse. The Republicans in charge of the committee should have held this hearing months ago instead of weeks before Americans pay their crushing first premium for January. Democrats on the Finance Committee have been ready to get to work for more than a year. When we first asked Republicans to confront this catastrophe facing American families. Instead of working to avoid these devastating premium increases for Americans, like our guests, Republicans devoted months to jamming through massive tax breaks for billionaires and, at the same time, cut more than a trillion dollars from the healthcare system that will result in 15 million people losing their coverage, hospital closures and higher costs for all, including those with employer-sponsored healthcare.

(03:37)

More than 160 million Americans are going to experience that cost shift in the form of higher premiums. Almost 70 million seniors on Medicare will pay a significant amount more for their Part B. Today marks the 421st day since the Finance Committee held a hearing on healthcare. This entire period, the Democratic position has been the same. Let's extend the tax credits and give our guests, Bartley Armitage and his wife, Carla Zimmerman, the same attention that the billionaires got so that middle-class folks can get ahead on their healthcare. So I say to Republican colleagues today, sitting on your hands has consequences. It's now the middle of open enrollment. Americans, like our guests from Eugene, Oregon, have already received alarming notices that their premiums are skyrocketing. In their case, by 500%, 500% to more than $2,200 a month. There is a health cost freight train, I would say to my colleagues, that's hurtling into view as we speak.

(04:46)

Based on what I heard on my trip back home to Oregon last week, more and more Americans are getting pushed onto those train tracks. Step one is to get them off the tracks. Open enrollment ends in less than four weeks from today for people who need their coverage to continue in January, like cancer patients or those with expensive prescription drug costs.

(05:08)

Step two is to address why Americans are in this predicament in the first place. That means reining in insurance company abuses across the healthcare system, not just for people who buy health insurance on their own. It means cracking down on middlemen who are skimming off the top of every single health expense, and it means taking on real fraudsters, like unscrupulous brokers or sophisticated corporate scammers who bill Medicare for billions each year. My own view, and I've looked at it, especially in the last few weeks, is there is no way for Congress to put together a proposal in the next couple of weeks that's going to help people in January.

(05:53)

Just can't be done. A clean extension this year is the bare minimum of what's necessary. If Republicans are ready to have the debate about what comes next, Democrats will say, "We have been waiting for it, we're ready to go." In the last several weeks, Republicans expressed a sudden willingness to take on big insurance. Now, I've been working on these issues for quite some time and I don't see any evidence of past history of Republicans taking on the big insurance companies.

(06:24)

So as we start this discussion, put me down as a bit skeptical. Now, if they are serious, serious about taking on the crooks that dominate big insurance like United Healthcare, I'm all in. In my view, that starts with a laser focus on lower costs for consumers, going after fraud where it truly exists and cracking down on middlemen. The fact is as we begin this debate, there is only one tough law on the books that really plays hardball with the insurance companies, and I'm proud to be able to say this morning, I'm the author of it.

(07:05)

It was a bill that dealt with the gaps in Medicare called Medigap. And when we started, seniors were getting ripped off every which way. They'd have fast talking salespeople come to their house and often sell them 8, 10, 12 policies that weren't worth the paper they were written on, weren't worth the paper they were written on. So I had seen this when I was Director of the Gray Panthers, but when I came to the Congress, I said, "Let's do something about it." And we played hardball with the insurance companies and now there's something that protects consumers and it protects the industry. So if you're serious about taking on big insurance companies, we'll have plenty to talk about, but I will tell you, I think that law is a logical foundation for addressing the healthcare challenges of our time. A couple of other quick points.

(07:58)

First, Republicans say the Affordable Care Act is all about fraud. The facts don't show that, but my view on that has always been any fraud is too much fraud. So in this Congress, I introduced a bill to rein in abusive practices by insurance brokers, like switching patients' plans without their permission. I thought we were going to get a bunch of Republicans. A lot of talk about fraud. The bill today is in the hopper. No Republicans want to fight fraud with us.

(08:29)

If Republicans are serious about helping patients get affordable healthcare, let's get serious about those kinds of frauds. Let me wrap up with a couple of points with respect to the Republican ideas I've seen floated in the paper, particularly ideas related to tax-preferred savings accounts. There is no question that these bills can be a useful tool for very wealthy people. There's no doubt about it. But I don't see it as a comprehensive health insurance opportunity for someone like my friend, Mr. Armitage.

(09:02)

Republicans make the claim that their ideas are going to deliver less money to insurance companies and more money to consumers. So our investigators spent the weekend looking under the hood and what we found is the number one administrator of these accounts is United Health Group and their subsidiary, Optum. Yet again, the big insurance companies have found a new way to profit off the system while lurking in the shadows.

(09:29)

So these proposals, right now, have an awful lot of Trojan horse in them for big insurance and they don't look to me like they're going to help Bartley and Carla. And my own sense is let's be on the lookout for somebody who wants to send a few thousand dollars to Americans and say, "That's going to take care of your healthcare and you can have that," rather than something that's going to help you pay for serious illnesses, like cancer.

(09:53)

Mr. Chairman, I'd like to enter a minority report on these tax schemes into the record.

Mr. Crapo (09:57):

Without objection.

Mr. Wyden (09:59):

Finally, there are a couple of other things we have to watch for. The very vulnerable people need a small dollar premium. Republicans have not been supportive of that. And finally, Republicans continue to raise additional anti-abortion restrictions that will pave the way for a de facto national abortion ban by inserting hide language into the tax code of America for the first time.

(10:24)

And I want to make the point now, very clearly, that on our watch, on this side of the dais, that's not going to happen. So there's a lot to do, but it's urgent business to pass a straight extension, now, so that Mr. Armitage and people like him can get some help. After that's done, I will be first in line to talk about bipartisan efforts to improve American's healthcare to lower costs, take on middlemen, rein in abuses of insurance companies. And I close, Mr. Chairman, as you and I have talked about and I've been interested in following up. Let's have more constructive debates like this.

Mr. Crapo (11:01):

Well, thank you, Senator Wyden. I will say that I'm not going to get into it. I disagree completely, well, almost completely with your characterization of the differences between us, but we will get into those and I hope we get to constructive engagement on these issues.

Mr. Wyden (11:14):

Wait till you see the names of the Republicans who stop the ripoff of the Medigap insurance by signing onto my bipartisan bill.

Mr. Crapo (11:23):

Okay, I'm not going to debate you on this right now, but let's just make it clear. We have been engaged very aggressively and we will continue to be very aggressively engaged. We have very big differences of opinion on these issues and we're trying to work out solutions.

(11:38)

I want to work in a constructive way, as you suggested, and we will try to make that happen. I have to go to a banking executive session right now, and so Senator Cassidy has said that he will do the introduction of the witnesses and get the process moving and I'll be back as soon as I can. Thank you.

Mr. Cassidy (12:00):

First witness is Douglas Holtz-Eakin, who serves as President of the American Action Forum. Prior to joining AAF, Dr. Holtz-Eakin was Chief Economist at the Council for Economic Advisors under President George W. Bush, and later, Director of the Congressional Budget Office. He has extensive knowledge of the tax code and health insurance markets and we're grateful for his input.

(12:22)

Next is Jason Levitis, is a Senior Fellow at the Health Policy Division at the Urban Institute. Prior to his current role, he served at the U.S. Department of Treasury under President Barack Obama. He represented the Treasury during the development, enactment of the Affordable Care Act, and we welcome his insights this morning. And I'm thinking, wait a second, am I introducing a Democratic witness?

(12:44)

And then lastly, Brian Blase is the President of Paragon Health Institute. Prior to his current role, he served as Special Assistant to President Trump at the White House National Economic Council. Notably, he was also staff for Senator Barrasso during his time as the chair of the Republican Policy Committee. Welcome back to the Senate. And now, I turn over to Ranking Member Wyden to introduce Mr. Armitage.

Mr. Wyden (13:07):

Thank you very much, Mr. Chairman. And Mr. Armitage, it's a pleasure to have you here. And Carla, I think, is right and back of you. And the two of you, as I was thinking about, are sort of the face of the healthcare challenge in America. One of the biggest hard-hit groups is folks between 55 and 65 and they're just praying that they can get through the hoops of healthcare, so they'll be eligible for Medicare at 65.

(13:38)

And you all were a few years short, you worked construction and the job was, as I understand it, grueling and sometimes physically brutal to you. And you did it for 40 years and you played by the rules and you worked hard and you were ready to have a bit of help for those couple of years until you were eligible for Medicare. And it just seems to me that this picture that you're going to paint today is especially important and I so appreciate your leadership.

(14:13)

When people hear what you all went through, they say that's what good citizenship and American values is all about. That's what you and Carla have been all about for decades, and I so appreciate you making the trek across the country. I know something about a number of subjects, but I know the airline schedules better than anything else under the sun, and it's a hard trip and I really appreciate you guys coming and it doesn't have to be this way. It doesn't have to be this way.

(14:44)

And I'm thinking about one thing, and it's what you said is, "Guys, stop fighting and figure out a way to help who are getting clobbered by these insurance costs," because that wrecking ball is headed your way and we're determined to figure out a way to get some help now. So you get through this and then work, as you've heard us talk about, on longer-term solutions. So glad you're here. Thank you for giving me the chance to introduce Mr. Armitage and Carla. Thank you for all the good counsel you gave at the various meetings where we talked about how you'd represent this incredibly important group of Oregonians and Americans, and thank you for your expertise on this subject as well. Thank you. Mr. Chairman.

Mr. Cassidy (15:27):

Dr. Holtz-Eakin.

Dr. Holtz-Eakin (15:30):

Mr. Chairman, Ranking Member Wyden, members of the committee, thank you for the privilege of being here today. In my testimony, I wanted to make three basic points. Point number one is that the ACA was and remains a flawed policy construct from several perspectives. As an insurance market, it's overly rigidly regulated, making it very difficult to manage the costs in that market, and it has proven to be a very high-cost location for insurance.

(15:59)

From the perspective of economic policy, it has some highly detrimental labor market incentives, both for the employers with the pay or play provisions, the taxes that were originally levied there and for the workers themselves where there's no tie between work and health insurance as there is with employer-sponsored insurance, which is a very important thing in America, to support work in every way that we can. And from the outset, the subsidies were so generous that you could do the math and figure out that up to 300% of poverty, it made a lot of sense for employers to just stop being in the insurance business, put their workers in the exchanges, and both the worker and the employer could come out ahead.

(16:40)

And so, those incentives were there at the beginning and they have not been changed. They remain, they are a headwind to ESI in America and to continue them and exacerbate them, I think, is unwise. And Senator Johnson is one of the people who did the original calculations on this, back at the launch of the ACA. And from a fiscal perspective at the time, I was quite worried about the implications for the budgetary outlook, which were not good then, are even worse now. And to add any further additional mandatory spending to the federal budget is simply unwise at this point and must be offset at a minimum or find another way to meet that objective. So as a piece of health policy, economic policy and budget policy, the ACA has always been a troubling construct. Point number two is that from the perspective of the 2026 plan year, the plans have been designed, the premiums have been set, many people have already enrolled and made their selections.

(17:35)

There's very little that this Congress can do to change the outlook. There are some channels by which you could get additional dollars to those participants in the ACA market. I'm happy to discuss those with you, but you can't do much to the fundamental working of the market at this point. Past 2026, within the constructs of the ACA, there are some options on HSAs, FSAs and other things that I'd be happy to discuss with you. They would be welcome changes, I think, and improvements in the ACA, but they don't change, fundamentally, the problems that we face in the healthcare area. And so point number three is we are overdue for a real rethinking of healthcare policy at the federal level, and I think there should be two primary objectives. The first objective would be to rationalize the insurance subsidies. We subsidize, essentially, every piece of health insurance in the economy.

(18:31)

Employer-sponsored insurance is subsidized through the tax code, through the non-taxation of it. We have the ACA subsidies, we have Medicaid, we have Medicare. All of these are on the taxpayer and they sometimes compete with one another. The ACA is just in competition with ESI and wherever the subsidies richer people can migrate. A rational set of subsidies that make sense from the perspective of the federal budget outlook and the needs in insurance markets would be a welcome change from where we are right now.

(19:01)

The second major objective is to get better incentives across the board for high-value care. It remains an objective that wasn't pursued very hard in the ACA at the time. There was a, are we going to cover everyone or bend the cost curve? And the ACA was about covering everyone, very little about bending the cost curve. We need to revisit that discussion and, in my testimony, I suggested that a great vehicle for you to think about improving those incentives is Medicare, Medicare Advantage in particular. That's the place where the majority of Medicare beneficiaries are. It has the greatest opportunity to influence practice patterns in the United States and Medicare is a great budgetary threat, and so I encourage the committee and the Congress, as a whole, to take a hard look at that and make some progress toward better healthcare outcomes and better budgetary outcomes. Thank you. Look forward to answering your questions.

Mr. Levitis (19:59):

Mr. Chairman, Ranking Member Wyden and distinguished members of the committee, thank you for the opportunity to testify about ways to make healthcare more affordable. My name is Jason Levitis and I'm a Senior Fellow at the Urban Institute. My views expressed here are my own and don't represent the institute, its trustees or its funders. I conduct research on the ACA and the intersections of healthcare and tax law. I also served at the Treasury Department, where I led ACA implementation and worked on tax-preferred health spending arrangements. Much of my focus, these days, is on how to simplify the healthcare system to reduce costs. The system has grown too complicated and segmented with a cathedral of complex rules. The Congressional Research Service recently cataloged 24 distinct varieties of tax-preferred health spending arrangements. This complexity increases costs for consumers, employers, and, ultimately, taxpayers. As we consider how to reduce healthcare costs, I'd love to partner with this committee on ways to simplify the healthcare system and related tax rules.

(21:04)

But my main focus today is more immediate. Open enrollment for 2026 is in full swing and millions of Americans are now seeing huge premium increases, people like Mr. Armitage. That's because the enhanced premium tax credits enacted in 2021 are expiring at the end of 2025. This will greatly increase costs for Americans. Premiums will increase for almost all of the 24 million people in the individual market. Premiums will more than double, on average.

(21:33)

4.8 million people will lose health coverage in 2026, exposing them to ruinous healthcare costs. These effects will be felt across all geographic areas, income levels and age groups. Certain groups will be especially harmed. Older people face the largest premium increases. People in high-premium areas will be hit hard. This is disproportionately rural areas. Self-employed people and small businesses often don't have access to group coverage and so rely heavily on the tax credits.

(22:03)

Among the lowest-income tax credit recipients, a person earning just $23,000 will have to pay a premium of about a thousand dollars per year in addition to deductibles and co-pays. The healthcare system overall is also in jeopardy. Together with the recent reconciliation bill, 14 million people will become uninsured, a 50% increase. This will reduce provider revenue by about $1.1 trillion over the next 10 years, risking a wave of hospital closures and other disruptions.

(22:34)

While the premium increases don't technically take effect until the end of the year, their damage has already begun and will grow with each additional day that an extension is delayed. That's because people are deciding, right now, whether to purchase healthcare for next year. The deadline to enroll is December 15th, less than four weeks from today. Already, millions are learning through notices or plan shopping that their premiums are skyrocketing. Many will drop coverage, choose not to enroll or cancel their automatic re-enrollment.

(23:03)

If they don't enroll, they will be ineligible for the tax credits, even if the enhancements are later extended. Others, especially those with pre-existing conditions, are making painful choices to re-enroll with the much higher premiums. They're cashing out retirement funds or foregoing dreams to start a small business, go to school or buy a house. A solution is needed urgently to stop this pain from spreading and start reversing it.

(23:27)

In recent days, we've seen a flurry of new ideas to change the enhanced tax credits or replace them with something else. It's certainly worth considering longer-term options to lower healthcare costs. Unfortunately, the calendar has overtaken the opportunity to implement such changes for 2026. The reason is simple. Putting in place a new policy would require months or years of implementation time. Setting aside the need to negotiate and pass a bill, any change would require marketplaces to build, test and deploy new IT systems.

(23:59)

Many would also require rulemaking and changes to state insurance regulations. By the time it's done, open enrollment will be a distant memory. So how can we stop this pain from spreading and start reversing it? At this point, the only feasible option is a clean extension of the existing enhancements. The marketplaces have already built to that option and have been preparing for months for the possibility of an extension. My understanding is that many marketplaces could update their systems for a clean extension within days.

(24:27)

I was working at the Treasury Department in those painful months in late 2013 when the marketplaces, having been rushed into services, to service, initially failed to function. That lesson should be heeded today. Building a new policy takes time. If rushed, it risks operational failure. The Senate Finance Committee is well suited to undertake a rigorous process to find bipartisan reforms for the future that get at costs and complexity, but these efforts will take months or years. For Mr. Armitage and millions more like him, the only help that can come in time is to extend the enhanced tax credits in their current form. Thank you.

Mr. Wyden (25:01):

Thank you. I share your view-

Mr. Cassidy (25:06):

Senator Blase. I mean, Dr. Blase.

Dr. Blase (25:08):

Not senator yet. Chairman Crapo, Ranking Member Wyden and members of the committee, thank you for the opportunity to testify today. The ACA promised affordable, high-quality insurance and it failed. Millions of families lost their health plans and doctors, premiums and deductible soared and networks narrowed. The law entrenched an inefficient insurance-dominated health sector with massive subsidies flowing straight from the Treasury to health insurance companies.

(25:42)

A new joint economic committee report found that the main winners from the subsidies are health insurers, whose stock prices have soared because of the ACA. The ACA's regulations increased premiums, nearly 50% in just the first year. Subsidies were needed so people could afford the more expensive coverage. The underlying regulatory and subsidy structure leads to ever-escalating premiums and prices. Since 2014, ACA plan premiums have increased nearly twice as fast as employer plan premiums. My family has an ACA plan.

(26:21)

We just received notice that our premium next year will be $33,000 for a plan with a $14,000 deductible. Higher premiums create pressure for still more subsidies. More subsidies lock in a high-cost system and permit large insurers and hospital systems to remain inefficient. If Congress wants to make healthcare more affordable, it must reform the structure itself, not throw more good taxpayer money after bad.

(26:52)

The ACA subsidies are ill-designed and inflationary. The enrollees' share of the premium is capped, regardless of the total premium. When enrollees pay only a small slice of the premium or no premium at all, insurers face almost no price discipline. Insurers can raise premiums knowing the taxpayers will absorb almost all of the increase. The ACA's regulations drive higher costs. For example, under the medical loss ratio, insurers must spend a minimum share of premium revenue on medical claims. In other words, to increase profits, insurers must increase premiums. The ACA's essential health benefits require plans to cover the same set of services, regardless of what people want or need. These rules increase premiums and wasteful spending. COVID-era subsidy boost resulted in fully-subsidized coverage and led to massive fraud. In 2025, there were 6.4 million people enrolled in fully-subsidized plans who are not eligible, costing $27 billion. Many of these enrollees were signed up without their knowledge or consent, victims of massive fraud schemes.

(28:04)

40% of fully-subsidized enrollees used no medical services in 2024. Federal taxpayers sent more than 35 billion dollars to insurers for people who did not use this plan a single time. The ACA subsidy structure, particularly with the COVID add-ons, incentivizes small employers to drop coverage. The percentage of small employers offering a health plan has dropped by one third since 2010. The ACA has also led some state and local governments to drop retiree health coverage, offloading that expense onto the federal taxpayer.

(28:43)

The COVID credits, by lifting the subsidy cap at four times the federal poverty level, provide large subsidies to wealthy, early retirees. ACA premiums will rise next year because of underlying flaws with the program. The large underlying subsidies will largely cushion the premium increase for more than 93% of enrollees. Most will pay less than $80 a month for a plan next year, with the federal taxpayer picking up 80% of the premium cost and a higher percentage for lower-income enrollees.

(29:14)

The Inflation Reduction Act set the COVID credits to expire after 2025, and they should end. Extending temporary emergency subsidies would deepen a broken system, instead of fixing it. The enhanced subsidies have supercharged fraud, benefited insurers more than patients and increased taxpayer exposure. In the near term, Congress should take three steps to help families. First, appropriate the cost-sharing reduction payments. This would lower silver plan premiums by roughly 12% and deficits by 30 billion dollars.

(29:48)

Second, give lower-income enrollees the option to take their CSR subsidy as an HSA contribution. Under an HSA option that Paragon developed, nearly 7 in 10 enrollees would be better off financially, with average gains of about $1,500 a year. This is exactly what we should be doing, redirecting existing subsidies away from insurers into accounts that patients control. Third, Congress should expand more affordable and flexible coverage options for families and small employers without new federal spending. Thank you and I look forward to answering your questions.

Mr. Cassidy (30:33):

Yes, sir. Mr. Armitage.

Mr. Armitage (30:38):

Good morning. Thank you, Chairman Crapo, even though he's not here, and Ranking Member Wyden for the opportunity to be here today. My name is Bartley Armitage. I live in Eugene, Oregon with my wife, Carla, who's sitting behind me. Carla was a teacher for 25 years. Together we raised our son and two daughters and now have three granddaughters, who we love to spend time with. Carla and I worked our entire lives. Our parents didn't have a lot of money.

(31:11)

My father died when I was 12 years old and my mother, my siblings and I lived in the basement of an old hotel for many years, as we were growing up. Counted on food stamps. Carla got her first job when she was just 13 years old and worked all through high school. I started working as a pretty small child, walking soybean fields with my grandparents on their farm and continued to work various jobs from then on. I moved to Oregon when I was 19 years old and spent nearly 40 years working various construction, but as a carpenter for 37 years, working my way up from an apprentice to a journeyman, then to a foreman, and finally as a superintendent

Mr. Armitage (32:00):

In charge of the contract for the company I work for. I was on a lot of major projects in that area with a lot of overtime. When you become a superintendent, you have to work a lot of hours, to say 10 to 12 hours sometimes just to get paid eight. Working construction takes a toll. I retired realizing I could no longer compete physically with 25-year-olds who were in their prime. For all my years in construction, I was worn out. You get worn out. I needed a couple knee surgeries and a hiatal hernia surgery.

(32:40)

Carla dealt with more demanding health issues, suffering from a chronic fever that we believe was caused by toxic black mold. She and our daughter spent years going from doctor to doctor trying to get a diagnosis for that. We ended up having to move out of our home. It still affects her today. My wife also had a necessary surgery several years ago that cost tens and tens of thousands of dollars just for a seven-hour hospital stay. Took us several years to pay off the debt that the insurance didn't cover. I can't even imagine what it would be like to navigate that situation without health insurance. Nobody wants to pay that kind of bill for one month. Most can't afford it. A bill like that is like having to pay for two houses.

(33:42)

Well, a bill like I will be looking at, which would be five times what I'm paying now. We're worried about having to deplete our retirement savings to pay for healthcare. We worked hard to raise three children, save that money, and on not really that great of an income. Our savings is what we plan to retire on and to have in case we need to eventually go to a nursing home and other things that could come up. It's there so we have a decent life and some of the things that nobody really wants to have to deal with. Since we shared our story, we have heard from so many people who are in the same boat as us, struggling to figure out how we're going to move forward with these costs. And before I conclude, Carla asked me to share a couple thoughts on her behalf.

(34:45)

First, of course, we want to be around to see our granddaughters grow up. Our fear is that without health insurance, we won't be able to go to the doctor if we're not feeling well, and face those consequences. We know people who haven't had the opportunity. And it breaks our heart to think about what they're going through, missing out on life because they couldn't afford to get the care that they needed. Second, making healthcare affordable for everyone is the type of thing we expect our tax dollars to go toward. In a country like the United States where it's a good country, it's a strong country, and it's a rich country, people should not have to go without care. I'm honored to be invited here today to share my experience on behalf of millions of other American families who are facing the same shock that we are. I urge you to take action that keeps our health costs affordable before we're hit with a massive bill like this January. It's literally overnight. Thank you. And I look forward to your questions.

Mr. Crapo (35:55):

I thank our witnesses very much for your testimony. I apologize. I had to step out to a Banking Committee for a markup vote for much of it, but I have read your testimony. And I'm very familiar with your statements and your perspectives. I'd like to start out, Dr. Holtz-Eakin, with you. Your testimony touched on the different ways that Congress could reimagine the complex network of the federal government healthcare subsidization put in place and also needed reforms for the Obamacare market. You further outlined various tax advantaged healthcare accounts and tools that already exist in the tax code, each with unique rules and benefits. Would you expand on the concept of delivering financial assistance through health savings accounts, especially for those enrolled in bronze and catastrophic plans?

Dr. Holtz-Eakin (36:46):

Certainly, Mr. Chairman. I think it's important to think about that in two different ways. The first is, as I said in my opening statement, for the 2026 plan year, your options are very limited. There are people who have enrolled. Then they have a bronze plan and an HSA. And you could appropriate additional funds to put in that to help them deal with the cost that they're facing in this plan year. But not everyone's got one, so you can't get to every beneficiary that way. So in the near term, it's fairly limited.

(37:20)

Beginning with the next plan year, that's an attractive policy because we've done some work. We have a micro-simulation model of the under 65 market. And if you put, for example, $4,000 in an HSA for everyone who has a bronze plan, you lower the cost compared to having premium tax credits. It's attractive from a budgetary point of view. You see obvious migration to the bronze plans and people using the HSAs to manage their finances. And you get reduced … Reductions in some of the premiums. So that's something that I think is worth consideration. I'd be happy to work with the committee with different variations on it.

Mr. Crapo (38:02):

Well, thank you very much. And Mr. Blase, you developed the concept of funding cost-sharing reductions, or CSRs, and depositing those dollars into a health savings account. I realize that's probably the Health Committee jurisdiction. But could you elaborate on this proposal? Could you also share with us information on how you would increase access to HSAs on the exchange?

Dr. Blase (38:24):

Sure. Thank you, Mr. Chairman. So the ACA had two subsidy programs. It had a subsidy program that reduced the amount of premiums for enrollees. It had a separate subsidy program for lower-income enrollees, which is about two-thirds of enrollees, that reduced their deductibles, co-payments, and out-of-pocket payments. The issue was the ACA wasn't written particularly well. And there wasn't a valid appropriation for the cost-sharing reduction program. So federal courts ruled that the Obama administration was making illegal payments through the CSR program. The Trump administration complied with that ruling. The CSR payments stopped. What insurers did in response was significantly increase the premium that the subsidy is tied to. So by doing that, premiums significantly increased and the premium subsidy significantly increased and the total subsidization went up.

(39:22)

What a CSR appropriation would do is significantly lower the benchmark premium, so silver plan premiums would come down 12%. And that would reduce the federal subsidies as well. So it's a way to lower premiums and reduce federal deficits by $30 billion. What we have developed with the HSA option is that enrollees, they would still get the premium subsidy, but they would be able to take the CSR subsidy under their control. They'd be able to get it as an HSA deposit. And Milliman analyzed the benefits of the HSA option and found that about 70% of enrollees would be better off if they took that, had the government subsidy into an HSA. And the annual benefit for them would be about $1,500.

Mr. Crapo (40:10):

Meaning that would be a much better solution for them than to have just a direct COVID era subsidy.

Dr. Blase (40:16):

That's right. It would replace the subsidy that goes directly to the health insurance company. And the individual would get the option to take that under their control as an HSA. And-

Mr. Crapo (40:26):

And you get that 12% reduction in the premiums.

Dr. Blase (40:30):

The 12% reduction in premiums would be silver plans across the board.

Mr. Crapo (40:35):

Thank you very much. And my final question for you, Mr. Blase, is you mentioned other ideas to increase affordability in your testimony. And these reforms are necessary to deliver broad-based diverse options for all Americans. The one-size-fits-all nature of Obamacare has been a significant driver of increased consolidation and decreased competition and choice. And I would just like you to discuss that concept very briefly. I'm almost out of time.

Dr. Blase (41:00):

Sure. So there's options that were developed in the Trump administration to help small businesses, to allow small businesses to join together through association health plans to gain the same regulatory advantages that large employers receive. It really doesn't make any sense that federal policy discriminates against small employers in favor of large employers. There's other options, like short-term limited duration insurance, which I know Idaho was very successful. In Idaho, that's comprehensive insurance, has much broader provider networks than ACA plans at a fraction of the cost.

Mr. Crapo (41:35):

Well, thank you very much. We appreciate your expertise here. Senator Wyden.

Mr. Wyden (41:41):

Thank you. Thank you very much, Mr. Chairman. Bartley, let me start with you. And you've been listening to this debate and getting a sense of all of these tax schemes that some of my Republican colleagues are talking about. When I listen to this, I don't hear much about consumer protection, but I see a real invitation to people like you to buy more junk insurance. And I heard you talking about the expensive illnesses that you and Carla had over the years. This junk insurance would just put you in a hole when what you're getting now allows you to stay in your home and pay for necessities until you're on Medicare. Am I missing something?

Mr. Armitage (42:32):

Yeah. We have paid a lot of medical bills over the years. We were able to manage them because we had insurance. Workout payment plans with the various health providers. And it cut into our budget tremendously at times, but we were able to manage it. And with the current budget that we have and the amount that we're paying now in 2025 with the high … We have a high deductible, so we still have to pay, but it's manageable. A lot of these ideas that I've been hearing about are … I don't have the depth to comprehend a lot of it, but I don't know. I'm pretty confused. And I'm concerned.

Mr. Wyden (43:26):

Okay. I'm concerned because I don't think it would come close to paying the kind of expenses that you and Carla had. And we'll talk some more about it, but that's what my concern is. How does it feel to be sitting there when the folks on the other end of the table in the suits are telling you when you ought to be allowed to retire?

Mr. Armitage (43:50):

Well, there are so many types of jobs in this world. Some jobs aren't as physically demanding. I work construction, various types of construction, roofing, glazing. And then got into the carpenter's apprenticeship. And it's very demanding physically, mentally as well, especially when you get into the managerial side of it. And it's a little bit like pro sports. The quarterback can't play till he's 45 years old. And in construction-

Mr. Wyden (44:22):

Brady thinks so.

Mr. Armitage (44:23):

Yeah. In construction, you have to cede to the younger generation at some point. So working till you're 66 years old isn't that feasible.

Mr. Wyden (44:36):

Yeah. Well, I just so appreciate you and Carla putting a human face on this because back here, everybody always talks about working families. If you had a nickel for every speech that featured working families, you'd be rich. But you all are talking about what it's really like. And I want to make sure you have good quality choices, not junk insurance. I've told my colleagues we did it once when it came to filling in the gaps in Medicare and not seeing seniors being ripped off anymore. So thanks for doing this, and so appreciate your talking about this. And look forward to … After the program, we'll get a sandwich. Thank you.

Mr. Armitage (45:17):

Thank you.

Mr. Wyden (45:17):

Okay. Mr. Levitis, let me ask you a question with respect to these tax issues. We have 24 health tax accounts now currently on the books. So there is a blizzard of all of these definite … This is a full employment program for accountants trying to make your way through this. And our Republican colleagues are now talking about number 25. They're going in the opposite direction for where I went with senior Republicans to make life better for folks trying to figure out how to buy Medicare supplements. Now, you've expressed the same kind of concern. Why are you so skeptical about the prospect of the 25th version of the same idea and somehow that's going to work out fine for everybody?

Mr. Levitis (46:08):

Thank you for the question, Senator. Well, so there are basically two reasons why, at this point, approaches like that just wouldn't do anything to help Mr. Armitage. The first is that it's just too late to build a system like that and have it in place for the marketplaces to work with the Treasury Department to transfer the money to the fiscal intermediary that runs these accounts for 2026. So time is just up for the immediate world for that options. But even beyond that, Mr. Armitage needs health insurance. And giving him a few thousand dollars in an account is not going to make a difference. He can't buy a short-term plan right now because he has pre-existing conditions. He won't even get the HSA because he can't afford a bronze plan. So these options right now just won't do anything for the affordability crisis.

Mr. Wyden (47:10):

Let me very, very quickly ask you for your thoughts on how you can take on big insurance in a way that tackles rising costs and reduces complexity without taking coverage away from people.

Mr. Levitis (47:25):

That's the great question. So I'll start by saying the Affordable Care Act did end some of the worst insurer practices in terms of discriminating against people with pre-existing conditions, but they have found other ways to not pay for coverage, things like prior authorization. And I think we absolutely need to look at ways to make sure that insurance companies are actually paying for the services that they should.

Mr. Wyden (47:55):

Why don't you give in writing your specific ideas? I share your view completely on fixing prior authorization. Thank you, Mr. Chairman.

Mr. Crapo (48:02):

Thank you. Senator Grassley.

Mr. Grassley (48:10):

I'm going to open with some remarks. Thanks, first of all, for the leadership of this committee for holding this hearing. It's a topic that's top on the minds of Iowans, high healthcare costs. It's kind of suffocating Americans for decades. One example occurs at the pharmacy counter. I've heard from countless Iowans that high prescription drug prices frequently lead folks to having to choose between paying for their prescription and other necessities. That's why, for years, I've worked to bring transparency and accountability to tactics deployed by the pharmacy benefit managers, or PBMs. And I'm not the only one in Congress doing it. In fact, the leadership of this committee is working on that as well. PBMs play a significant role in the pharmaceutical drug supply chain. They act as middlemen, processing prescriptions, negotiating prices, setting formularies. My bipartisan legislation would increase transparencies to better hold PBMs accountable.

(49:32)

While not wholly within the committee's jurisdiction for my legislation, I hope my colleagues will see the importance of acting on PBM reform as soon as possible. High prescription drug prices are one of the several factors driving up healthcare costs. The rising cost of healthcare is also evident from escalating health insurance premiums and required co-pays. There are many parallels between the conversations we're having today and the ones that I had with my Senate colleagues back in 2009. Unfortunately, my colleagues on the other side of the aisle [inaudible 00:50:13] Obamacare on a partisan basis. At the time, my democratic colleagues claimed the law would bend the cost curve down. It's now evident that that was false, as was the promise that individuals could keep their health plan if they liked it. Since the enactment of Obamacare, millions of Americans have been thrown off their preferred health plan, while health insurance premiums have skyrocketed. According to Paragon Institute, since 2014, Obamacare benchmark premiums have increased 129% for a 50-year-old enrollee.

(50:59)

Obamacare premiums have increased twice as fast as premiums for employer-provided coverage and three times faster than inflation. That leaves us here today revisiting the debate on ways to bend the healthcare costs curve. We need to find a solution that will allow all Americans to breathe a little easier when they seek healthcare, while also ensuring those with pre-existing conditions are protected. So Mr. Holtz-Eakin, I've been a proponent of shining light on healthcare costs, providing businesses the opportunity to help their employees get health insurance, and allowing consumers the ability to shop for options. You recently expressed concern that some of the new mandates around drug pricing, surprise billing, and transparency can add burdens, which may erode, quote … I want to quote. " The comparative advantage of the private market," unquote. I'd like to have you elaborate on the factors Congress should consider as they seek to promote greater healthcare transparency and competitive private insurance market.

Dr. Holtz-Eakin (52:17):

I'm not exactly sure where that quote's from, but the general concern is mandates as opposed to transparency, restricting the ability of the private sector to effectively respond to incentives to control costs. That's been my concern with the ACA from the outset. It was a heavily one-size-fits-all rigid mandate-driven system. Making it more transparent as to how it works, I don't think changes that. And so I think, as I said in my written testimony, a way to get better health policies, actually remember that the delivery of insurance devices, drugs, medical services, is an economic activity. And we should have the same standards for good economic policy in health as we have elsewhere. And that includes keeping taxes low and on broad-based and keeping regulations efficient and targeted on real problems. I'm just worried about an excessively regulatory approach.

Mr. Grassley (53:19):

I'll have to submit the rest of my questions [inaudible 00:53:22].

Mr. Crapo (53:21):

Thank you, Senator Grassley. Senator Cornyn.

Mr. Cornyn (53:26):

Thank you, Mr. Chairman. Dr. Holtz-Eakin, I think our national debt is approaching $38 trillion.

Dr. Holtz-Eakin (53:34):

Yes.

Mr. Cornyn (53:34):

And we're paying more money on interest on the national debt than we are on defense of the nation.

Dr. Holtz-Eakin (53:40):

That's correct.

Mr. Cornyn (53:40):

Which strikes me as unsustainable. I hear proponents of the status quo, these very expensive ACA subsidies saying we should just keep using more tax dollars to subsidize insurance companies and not look at reforms of the current system. I'm struck by Mr. Heritage's … Armitage's, excuse me. Mr. Armitage's testimony. And obviously, we want to make sure everybody has access to healthcare in America. But I also recently was talking to a young man, who happens to work in a barber shop in Austin, Texas. And I said, "Where do you get your healthcare coverage from?" He said, "Well, my employer provides it." He said, "But I don't take advantage of that." I said, "Oh, you want the cash instead?" He said, "Yeah. I'm 40 years old. I'm healthy. And I'll take my chances." But it strikes me as that we're talking about a nation of 330 million people. We're talking about a population of roughly 24 million that are on these ACA policies.

(55:04)

And the federal government under the ACA treats everybody the same. And we've used the phrase one size fits all. But isn't it true that the needs of individuals are not accommodated by a one-size-fits-all policy and that consumer choice might be a pretty good alternative and one that would be more economically sustainable?

Dr. Holtz-Eakin (55:29):

I completely agree with that, sir.

Mr. Cornyn (55:32):

And Dr. Blase, you've documented the incredible enrichment of insurance companies. I'm not sure people really have figured this out. So the money from the federal government goes to the insurance company. And are they incentivized to sign up as many people as they possibly can?

Dr. Blase (55:51):

Yes, Senator. The subsidies almost entirely are payments directly from the Treasury to the health insurance companies. And they have been the beneficiaries of a lot of this significant fraud and improper enrollment because they're enrolling people that many times don't know they're covered by the plan, that don't use the insurance at all. So the government is sending massive payments to insurers on behalf of people who just don't use the plan ever.

Mr. Cornyn (56:18):

Well, wait a minute. So could somebody could be covered by an ACA policy and not even know it?

Dr. Blase (56:26):

Yes.

Mr. Cornyn (56:27):

How does that happen?

Dr. Blase (56:28):

So when these subsidy enhancements were put in place, they made the coverage fully taxpayer subsidized for a share of the population. That set in place sort of a massive set of fraud schemes throughout the country to manipulate applications to give people the appearance that they could get a cash gift card if they called a number. They called the phone number. They were asked if they wanted to sign up for health insurance. First, they gave their name, date of birth. They got enrolled in a health insurance plan. But they then would call back a few weeks later and ask about their cash gift card. There's a Bloomberg story from June that quotes one of the customer service agents. It says half of the people that we enrolled had no idea that they were signing up for health insurance. And they don't pay any premium, so they don't see the payment. The subsidy just goes directly from the Treasury to the insurance company. And we've been automatically re-enrolling people year after year through this system.

Mr. Cornyn (57:33):

And what I hear my democratic colleagues saying is we need to stay the course in this system. But who's paying the premiums for those people who don't even know they've been signed up on ACA?

Dr. Blase (57:44):

The taxpayer is paying the full premium. And the ACA overall, now, 85% of the revenue that insurers collect comes from the federal taxpayer. So the insurer main client is the federal taxpayer.

Mr. Cornyn (57:59):

And is the fact that 40% of the enrollees in fully subsidized plans did not file a single claim, is that also an additional data point or piece of evidence indicating that people have been signed up by these insurance companies and these head hunters, I'll call them, who get paid a commission presumably for as many people as they can sign up as possible? That all of those people, or many of those people, did not even know that they were enrolled in a plan and taxpayers are subsidizing it?

Dr. Blase (58:34):

Yes, Senator. I think it's one of the best data points to illustrate the problem. In August, CMS released data for people that didn't use their health plan a single time. And of the fully subsidized enrollees, 40% of them didn't use their health plan a single time. Now, in health insurance, most people use their coverage during the year. 85% of people with a health plan. Because we spent … So much of our health spending goes through our insurance that it's rare for people to have a health plan and not use it. But in the ACA, it's becoming more the norm with all of these subsidies going to insurers that people aren't aware that they're enrolled in the coverage.

Mr. Cornyn (59:15):

I see my time's expired. Thank you, Mr. Chairman.

Mr. Crapo (59:18):

Thank you. Senator Bennet.

Mr. Bennet (59:20):

Thank you, Mr. Chairman. And thank you for the witnesses for being here. Mr. Chairman, you said at the outset of this hearing, I think, an extraordinary thing for the Chairman of the Senate Finance Committee in the time that I've been here, and that is that the American healthcare system is broken. That's an emphatic statement. And it's a statement that I completely agree with. And from the standpoint of the people that I represent in Colorado where they're suffering day after day after day with the effects of a system that costs them twice as much as the healthcare system of any other wealthy country, any other industrialized country in the world, a system that provides them so much less than those other healthcare systems around the world are providing, I could not agree more with that observation.

(01:00:15)

And other countries that we compete with that are spending half what we're spending on healthcare. And the half is the federal government. The half is small businesses. The half is families that are all spending twice as much as other industrialized countries around the world. In those other countries, they expect, as a right, access to primary care, access to mental healthcare, access to maternal care, access to affordable prescription drugs. President Trump has talked about that over and over again. Hospitals that have enough doctors and enough beds and enough time for somebody who's gotten sick to actually spend time there and get well. A lot of times in life, you pay a little, but you get a little. There are rare moments in life, I suppose, when you pay less and get more. But that's true of people that are living in these other healthcare systems. And I think the immediate task before us is to extend these tax credits for the Affordable Care Act. We have to do that because otherwise, in our states, people are going to see increases of 200% for healthcare, 300% for healthcare, 400% for healthcare. In rural and urban Colorado, in rural and urban America, that is what they're going to face because of the negligence of people in Washington that are now discovering that our healthcare system is broken. But that's not going to fix our system. That's just going to save people from going bankrupt in the short term. We've got to fix the system that we have.

(01:02:01)

And when the Affordable Care Act was coming through here and we were trying to regulate the insurance companies by saying, "You can't throw off Americans because they have a pre-existing condition. You can't throw off Americans because they have cancer," these guys were all against that because we were regulating the private insurance company in America, and that that was going to be bad. And now they're here to say the private insurance company is this fraud scheme. That's also an amazing thing to hear on the Finance Committee, but it's welcome, from my perspective. And I'll be honest about it. I support a universal healthcare system in America. I think we should have a universal healthcare system in this country because I think the American people deserve to spend half of what we're spending on healthcare and get a better result.

(01:02:54)

I think people in Colorado deserve to have the chance to have mental healthcare for their children, just like people across the industrialized world, rich countries around the world that are not infected by the special interest politics that have driven drug prices through the roof, that have driven insurance prices through the roof, that have caused us to have a system that rewards over and over and over again, to Doug Holtz-Eakin's point, fee for service, fee for service, fee for service, pay as much as possible, instead of putting us in a system where we can actually take better care of ourselves and live better lives and live longer lives.

(01:03:39)

Do you know that the average life expectancy in this country is six years less than in those other countries that have systems of healthcare that cost half as much? And I don't have time. And let me just finish by saying I don't think the answer here is a command and control answer from Washington DC.

Mr. Bennet (01:04:00):

… you see, quite the opposite. I think we should give everybody in America a public option that is administered by Medicare that gives every family in America the chance to decide whether they can get out from underneath the insurance industry that you're talking about. Getting in a plan where they can actually see the benefit of being in a place with managed care and the chance to be able to take better care of themselves. And be rewarded for that instead of be at the whim of the drug companies than the whim of the insurance companies. Mr. Levitis, in my last five seconds, do you have anything you'd like to say about that?

Chairman (01:04:41):

Briefly, please.

Mr. Levitis (01:04:45):

Very briefly. I would be happy to say that yes, insurance is not perfect, but people need insurance and we need to make it affordable for people. And whatever flaws it has, we shouldn't punish the people who need insurance by not making it affordable for them.

Mr. Bennet (01:05:02):

Exactly. Let's fix the system before we double, triple and quadruple the prices on the American people. Thank you.

Chairman (01:05:12):

Senator Cassidy.

Senator Cassidy (01:05:13):

First, let me remark that I think there's remarkable agreement between Democrats and Republicans. Obamacare failed to give access to all Americans to healthcare and Obamacare failed to control healthcare costs. And the kind of comments that have been made back and forth make that clear. The question is how do we address this? And this is personal to me. I'm a physician who worked for 20 years in a hospital for the poorly insured and the uninsured. Sir, your story about your issues or the patients that I used to see, and one thing you've mentioned, if not emphasized, but I happen to know that deductibles which are too high become a barrier to accessing the insurance.

(01:05:52)

You are someone, we need to do something for your insurance policy, not just the deductible but also the cost of the premium itself. I think that's true. Now we also have to control healthcare cost. So Dr. Blase. I got limited time. Be tight man. Be tight. So tell us about the ability of a health savings account just statistically, not your opinion, but what statistics show that once you give the mama the power of the purse, the ability to shop with a health savings account in which she's awarded if she chooses a lower cost option. What impact does that have on healthcare cost?

Dr. Blase (01:06:25):

Yeah, I mean you can look at a 15 to 25% reduction, senator.

Senator Cassidy (01:06:28):

A 15 to 25% reduction in what?

Dr. Blase (01:06:32):

In the overall healthcare spending for that family.

Senator Cassidy (01:06:35):

And does it negatively affect outcomes, which is to say do they end up as healthy as they would've?

Dr. Blase (01:06:42):

They end up just as healthy as before. It turns out that when they have that control, Americans can be wise consumers and make good decisions about what's in the best interest their health.

Senator Cassidy (01:06:51):

Americans can be wise consumers. You're telling me that we can actually trust that mother, that wife and women make almost all the healthcare decisions. We can trust her to make a wise decision. We don't have to be paternalistic.

Dr. Blase (01:07:01):

I agree with that Senator. Yes.

Senator Cassidy (01:07:03):

And by the way, there's more importantly that has been pointed out by study after study. Now Dr. Holtz-Eakin, we keep making the point. I'm so impressed that my colleagues are so want to give the money to the insurance companies, but can you explain briefly the medical loss ratio that allows 20% of the money that we give to insurance companies to be used for profit and for overhead as opposed for direct medical care.

Dr. Holtz-Eakin (01:07:32):

In the ACA, the medical loss ratio dictated a minimum amount, 80%, 85 in some cases that had to be spent on medical care as opposed to other uses of it by the company profits, administrative expenses.

Senator Cassidy (01:07:48):

So under the Affordable Care Act, I think it's 20% is allowed to be taken by the insurance company, not for healthcare but for overhead and for profit.

Dr. Holtz-Eakin (01:07:58):

Correct.

Senator Cassidy (01:07:59):

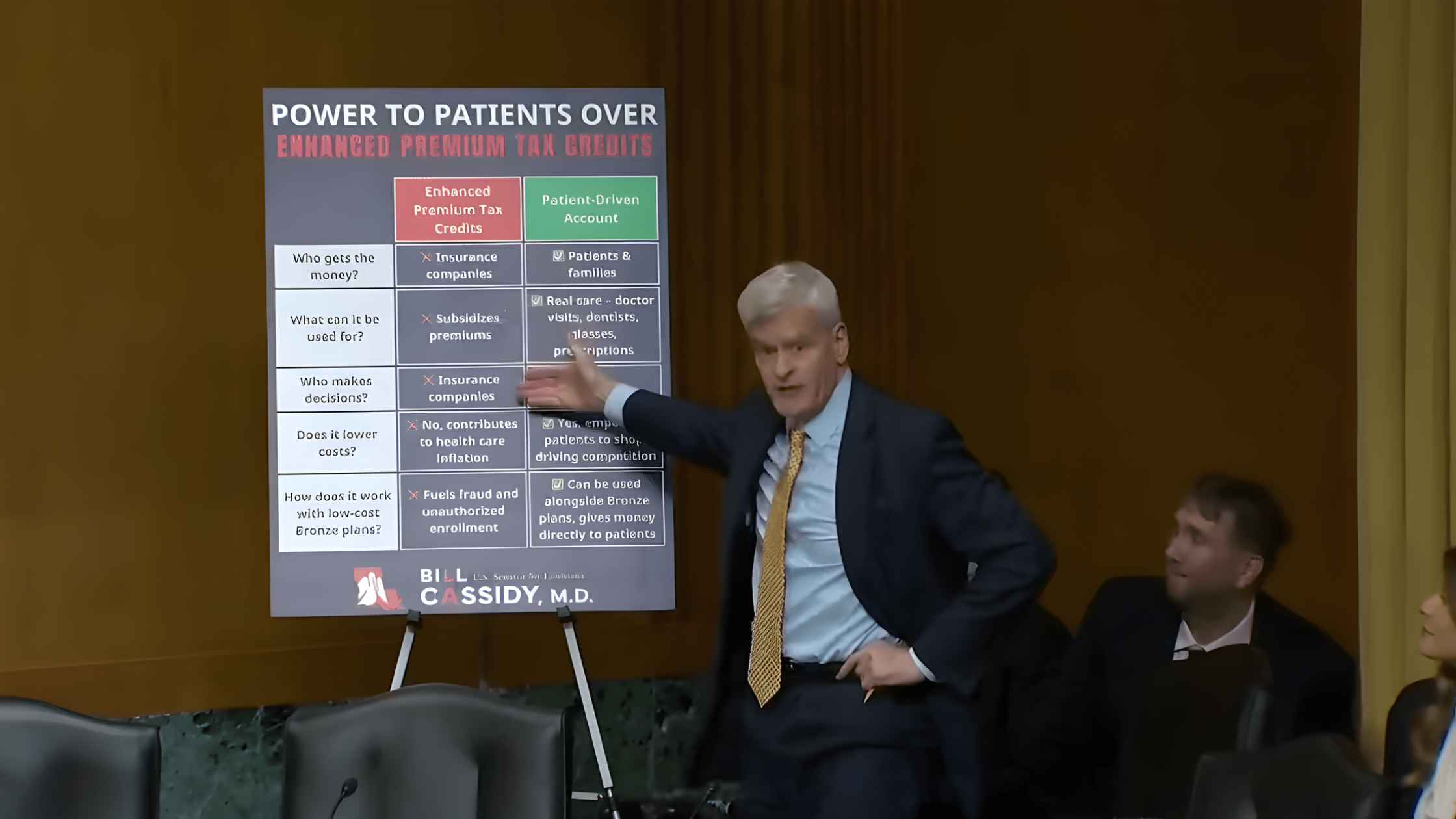

Now, as a guy who wants all the money to go to the patient because we found that the patient can be trusted to make wise decisions, the fact that we are like giving 20% for overhead, and we need insurance companies, but 20% for overhead and profit, that's 20% wasted on direct care. Can you put up my poster please? I want to demonstrate this right there. If you see under the status quo that my colleagues are pushing, 20% is going to the insurance company for overhead and for profit. 80% for the healthcare that the insurance company believes that the patient needs and she can't get it unless they agree. And under what we're proposing is that 100% goes-

Speaker 1 (01:08:42):

That Pastor Reggie Miller definitely bribed the refs. It was obvious-

Senator Cassidy (01:08:48):

Senator Wyden, will you turn off your phone please.

Chairman (01:08:50):

He's trying.

Senator Wyden (01:08:51):

Technology.

Senator Cassidy (01:08:53):

100% goes to a patient-driven account in which you can use for a physician or dentist or drugs. 100% goes. Now that's really the choice we have here. Now can we put up the next, and let me just do a side-by-side of what we're talking about because to believe this, I am asking that we move from our entrenched positions. Right now it's like trench warfare. If a Republican proposed it reflexively Democrats opposed and vice versa. If we're going to get something that works for you, sir, we have got to move beyond being a D or an R into something in which we're first an American. So let me do a side-by- side. Under the status quo the insurance companies get the money that subsidizes premiums. The insurance company makes the decision and it doesn't lower healthcare costs. In fact, it actually contributes to higher cost and it fuels fraud and unauthorized enrollment. For the record, I'd like to submit an article showing that there's a $233 million penalty levied upon insurance brokers fraudulently enrolling people in zero-premium policies-

Chairman (01:10:01):

Without objection.

Senator Cassidy (01:10:02):

… under what we're supposing what we're proposing. And I ask my democratic colleagues to think about it, just don't be entrenched. Think about it. In which the money goes and is controlled by the patient, the family for real care, for the dentist, the physician, that a patient makes the decision. It empowers the patient to lower the cost and Dr. Blase points out that that has been established by studies and it can be used alongside a bronze plan. We've heard criticism this would take too long to implement. I will point out that under the One Big Beautiful Bill, Congress established already under law that bronze plans can use HSAs. I'm out of time. I'll stop. With that, thank you.

Chairman (01:10:47):

Thank you very much. Senator Whitehouse.

Mr. Cornyn (01:10:51):

Thanks Chairman. I think we know a fair amount about what works and what doesn't work. One thing we know is that fee-for-service doesn't work and the quicker we move off fee-for-service to value-based programs, the better. We had some good experience after the Obamacare bill with the accountable care organizations, which have worked extremely well and enjoyed bipartisan support and been successful in red and blue states alike. So there's one. I think the other area worked with Senator Cassidy on this is that the specialists have too much control over what gets charged and letting primary care doctors make more decisions and specialists make less about who gets paid what looks like it would reduce costs.

(01:11:38)

We have specific experience in Rhode Island that confirms that. A third thing that is a real pain in the neck for people and also a cost driver is prior approvals. Why would you let an insurance company require prior approval before they let a doctor go forward with care that you need? And in particular, why would you do that when the doctor is not on fee-for-service when the doctor is moved to value-based care? There's at least an argument that in a fee-for-service world you could have doctors churning and churning and churning and churning the meter to get that nonsense out of the system. That's a huge part of that 20% overhead cost, which by the way was something that Democrats fought to reduce to 20%, which by the way was something that Democrats fought to reduce to 20% against pressure from the other side.

(01:12:27)

But immediately we have a problem of people who have an immediate concern for their livelihoods and for their financial well-being. I talk a lot, Mr. Armitage, about Carla in Rhode Island who is a retired mental health counselor. 60K annual income, doesn't qualify for Medicare yet and gets her health insurance through our health insurance marketplace. Her premium is going to increase from $427 to $ 904, a 112% or $477 per month increase. That is an immediate problem that we can solve by extending the affordable care credits while we have this larger discussion about how to bring things down. Mr. Armitage, how do you feel about the problem of the individuals who are about to get whacked with a hundred percent increase because Congress has failed to extend these credits?

Mr. Armitage (01:13:30):

Well, I really appreciate the discussion about how we can improve the health insurance in the future, how it can reduce the cost. I like what Senator Bennett had to say about nationalizing healthcare, but my immediate concern is January 1st, 2026 when my payment, my wife and I are paying $443 a month and on January 1st, if we continue that, we will be paying $2,224 a month. That's 500%. So I would hope that we can fix this problem that we've had in this country for a long time. I used to have good insurance when I was a working carpenter. I couldn't continue that, unaffordable to continue that after retiring. My wife had good insurance while she was working. She can't continue that after retiring. It's too expensive. And now we're faced with very expensive, but we need time to make this transition, I think.

Mr. Cornyn (01:14:38):

But you need a response before January 1st when you're premium quintuples.

Mr. Armitage (01:14:44):

Exactly.

Mr. Cornyn (01:14:45):

And Mr. Levitis behind, Mr. Armitage's problem is a problem of the healthcare system that is suddenly going to be starved of revenue, nursing homes, hospitals, provider practices. What does that look like behind Mr and Mrs. Armitage's problem?

Mr. Levitis (01:15:04):

Thank you for the question, Senator. So that's exactly right. Between these premium increases and what was in the reconciliation bill, we're seeing over a trillion dollars of federal support coming out of the healthcare system going to providers, which is going to mean more hospitals closing and other stresses and disruptions in the system.

Mr. Cornyn (01:15:24):

Known. Known, right? We're doing this and we know it. So please, let's get this fixed before that happens. Thank you, Chairman.

Chairman (01:15:34):

Thank you. Senator Daines.

Senator Daines (01:15:36):

Mr. Chairman, thank you and thanks for holding this important hearing. At the center of this discussion today is the future of the expiring Obamacare COVID era subsidies. It's important to note that Democrats establish these enhanced subsidies on a temporary and purely partisan basis during the pandemic. Under President Biden and elected to have them expire at the end of this year. I remember distinctly going back in time when Obamacare passed, when President Obama said is going to lower, it's going to lower premiums by $2,500 a year. And we've seen certainly a cause and effect. We put in place Obamacare and now we've seen healthcare in the exchange, which about 7% of the American people receive their healthcare that way becoming completely unaffordable. Basically by the way we predicted that and sadly that has come to fruition. We've got to deal with this. The current situation is entirely of the Democrat's own making and Republicans and frankly both sides of the aisle should not perpetuate the mistakes that accelerated Obamacare's failures. Debate over the temporary COVID subsidies reveals a core underlying reality. More than a decade after its implementation, Obamacare remains unaffordable, fundamentally broken and increasingly reliant on massive recurring taxpayer bailouts. The expiring pandemic subsidies bear little responsibility in the 20% average premium increase in non-group Obamacare plans for '26.

(01:17:24)

But they do bear responsibility for distorting the market, increasing fraud and abuse, making Obamacare more dependent on taxpayers, raising healthcare costs over the long term and worsening our budget deficit. In fact, making the enhanced subsidies permanent would cost taxpayers nearly $400 billion amounting to a massive transfer of taxpayer dollars to insurance companies. I believe any path forward in this issue requires reforms. Reforms that address the root causes of why does Obamacare perpetuate high costs and instability as well as the substantial growth in improper enrollment, in fraud and in wasteful spending. In addition to permanent structural reforms to Obamacare, any path forward should expand access to and unleash free market patient centered solutions that President Trump championed during his first term, provide lower costs, more control and better care for individuals.

(01:18:40)

I think both sides should agree we need that and we need it badly. Obamacare also represented a substantial departure from the hide amendments prohibition on taxpayer funding of elective abortion. It is imperative that any reforms explicitly restore the long-standing consensus that taxpayer dollars should not subsidize and facilitate health plans that cover elective abortions. Dr. Blase, as you noted in your testimony Obamacare has worsened the quality of individual market health insurance, substantially raise premiums and deductibles and costs taxpayers hundreds of billions of dollars. In your view, what structural reforms to Obamacare would lower premium costs and reduce some of these inflationary pressures?

Dr. Blase (01:19:34):

Yeah, thank you for that question, Senator Daines, and I agree with your view that there are deep structural problems in Obamacare. The worst thing that Congress could do is just to perpetuate the inefficiencies for insurance companies, for big hospital systems by further putting taxpayer dollars in place. We need to look at alternatives. So you mentioned alternatives that the Trump administration opened up for small businesses to join together and get the regulatory advantages that large businesses receive short-term limited duration plans, which are much more affordable and flexible.

(01:20:09)

My family was enrolled on a short-term plan for a year and within the ACA structure itself to look at the regulations that drive up the cost of premiums. One of them is the medical loss ratio, but the underlying subsidy structure is also inflationary. The subsidy holds the enrollee harmless from any premium increase. So insurers are pricing knowing that the entire premium increase over time is borne by the taxpayer, that gives insurers enormous power to inflate premiums over time rather than provide value. Ultimately we need to construct a system where the insurer is providing products that the patient values rather than just coming to Washington and lobbying for more federal dollars.

Senator Daines (01:21:00):

To place. Thank you.

Chairman (01:21:03):

Thank you. Senator Cantwell. Okay, Senator Smith.

Senator Smith (01:21:12):

Thank you Mr. Chair. So there have been lots of conversations today about what we can do theoretically to lower healthcare costs and I am all in on having these conversations. And it's also really clear from this hearing that republicans really don't like Obamacare, even though most Americans strongly support the insurance reforms in Obamacare and what it's done to get more people covered. But I think we need to be real colleagues about where we are right now. After all this back and forth, it's clear to me there is one way and there is only one way that we can keep Americans health insurance premiums from skyrocketing come January 1st. And that one way is to extend the affordable care tax credits. That's the only option that we have on the table. And I think it's a good option.

(01:22:06)

And Democrats have been ready to do this for months, but President Trump and Democrats are saying no. And in fact last night, president Trump said on truth social all caps, "The only healthcare bill that I will support or approve is sending money directly to the people with nothing going to the big fat insurance companies." So let me just dive into that for one minute. Mr. Levitis, I want to ask you this, the president Republicans are proposing, as best I can tell, sending money to Americans and basically saying, "Forget about insurance, we're just going to send you money and you can buy your healthcare." So what would that look like if we actually did that? And people who aren't worried about their healthcare end up leaving the insurance markets.

Mr. Levitis (01:22:49):

So it would mean two things. First of all, it would mean that people like Mr. Armitage couldn't afford the health insurance that he needs. And then second, it would mean that premiums went up for everyone. And so other people-

Senator Smith (01:23:03):

Would only increased costs, right?

Mr. Levitis (01:23:04):

That's right.

Senator Smith (01:23:05):

Right. And Mr. Armitage, I appreciate your testimony so much and thank you for being here. You and your wife have spent years as you've told us, paying off your medical debt. So if you got a check for $6,500 or even a little more than that, would that have solved your issues with medical debt? Would that have made all your problems magically go away?

Mr. Armitage (01:23:26):

Did you say 5,500?

Senator Smith (01:23:28):

65.

Mr. Armitage (01:23:30):

65. It would be a down payment on a long-term cost when insurance is so expensive. Without any help, it would be a few months.

Senator Smith (01:23:44):

A few months

Mr. Armitage (01:23:45):

And then what? Then we're right back. This is ground zero.

Senator Smith (01:23:48):

Right. And then you're faced with trying to figure out how to… You can't afford your life if you don't have health insurance.

Mr. Armitage (01:23:53):

In a couple months maybe I don't need much medical care. So I'm basically turning the money right back over to an insurance company, back to ground zero, no help, no ongoing protection or insurance affordability.

Senator Smith (01:24:13):

Thank you for that. And there's another issue that has not really been discussed very much today, but I bet it would come as a big surprise to a lot of folks if you're listening to this hearing that behind the scenes part of what's going on here is actually a big debate about abortion. You're like, "Really? I haven't heard that much about this topic today." But what is really happening is that Donald Trump and Senate Republicans are insisting, they're saying, "We won't agree to lower your healthcare premiums for millions of Americans unless they can get a ban on private insurance covering abortion care." So let me just go to you on this Mr. Levitis, because I think there's a lot of misinformation out here. What is going on here is they're saying, "We won't help you afford your health insurance unless we can mandate what kind of health insurance you can buy with your own money." So under federal law, can federal funds be used to pay for abortion care?

Mr. Levitis (01:25:09):