Policy Limit Investigations + How To Maximize Recovery

Understand policy limit research in personal injury cases and learn how to identify coverage, strengthen strategy, and maximize recovery.

In personal injury cases, potential settlements are rarely what they seem at first glance. But, if you put the defendant’s insurance coverage under a microscope, you’ll often discover a complicated collection of policies and players — and the possibility of settling for much more than initially thought.

This is why policy limit investigations are such a central component of PI case strategy. They help attorneys move beyond surface-level disclosures to identify every available source of recovery, from primary policies to excess coverage and third-party liability.

Done well, these investigations can shape how a case is valued, negotiated, and ultimately resolved. Here’s how insurance policy limits investigations work, where they sometimes fall short, and how to use them to maximize recovery.

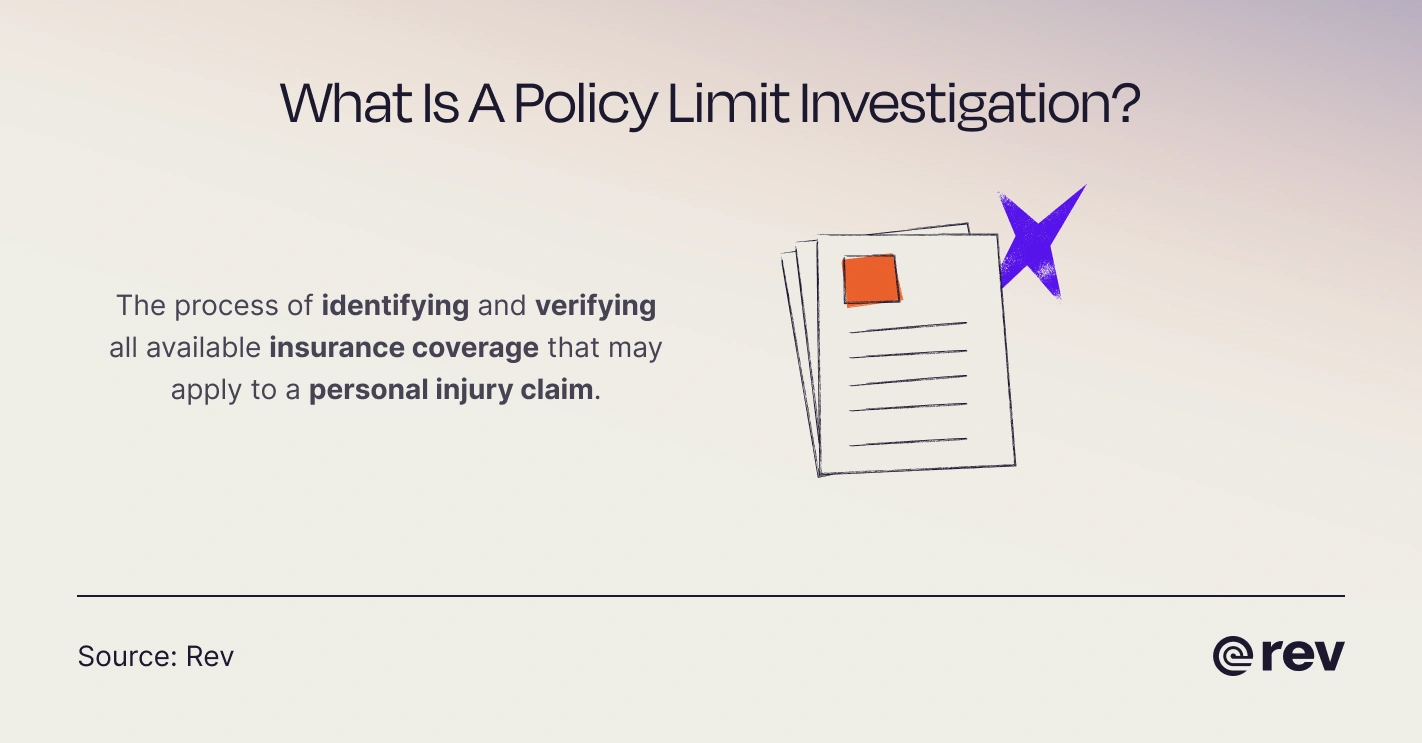

What Is A Policy Limit Investigation?

A policy limit investigation is the process of identifying and verifying all available insurance coverage that may apply to a personal injury claim, including the limits, layers, and conditions of those policies. Because insurance policies are legally binding agreements, they function as a specific type of contract that defines what is (and isn’t) covered and how much can be recovered.

Attorneys typically begin combing through these agreements early — often during intake and pre-suit investigation — and continue through discovery to confirm whether coverage goes beyond what was initially disclosed.

These investigations are critical because the defendant’s insurance coverage (rather than their bank account) often represents the primary or only source of recovery. As a result, understanding policy limits can affect everything from case valuation to settlement strategy. In some cases, it may even create leverage for potential bad faith claims if an insurer fails to settle within those limits.

“Sometimes your opposing party tries to play hide-the-ball with the limit of the insurance policy, and determining that limit, where the defendant has no or little resources to recover from, is key in a personal injury case,” says attorney Jennifer Duffy of Duffy Law. “It really determines whether the lawyer will undertake the case or not.”

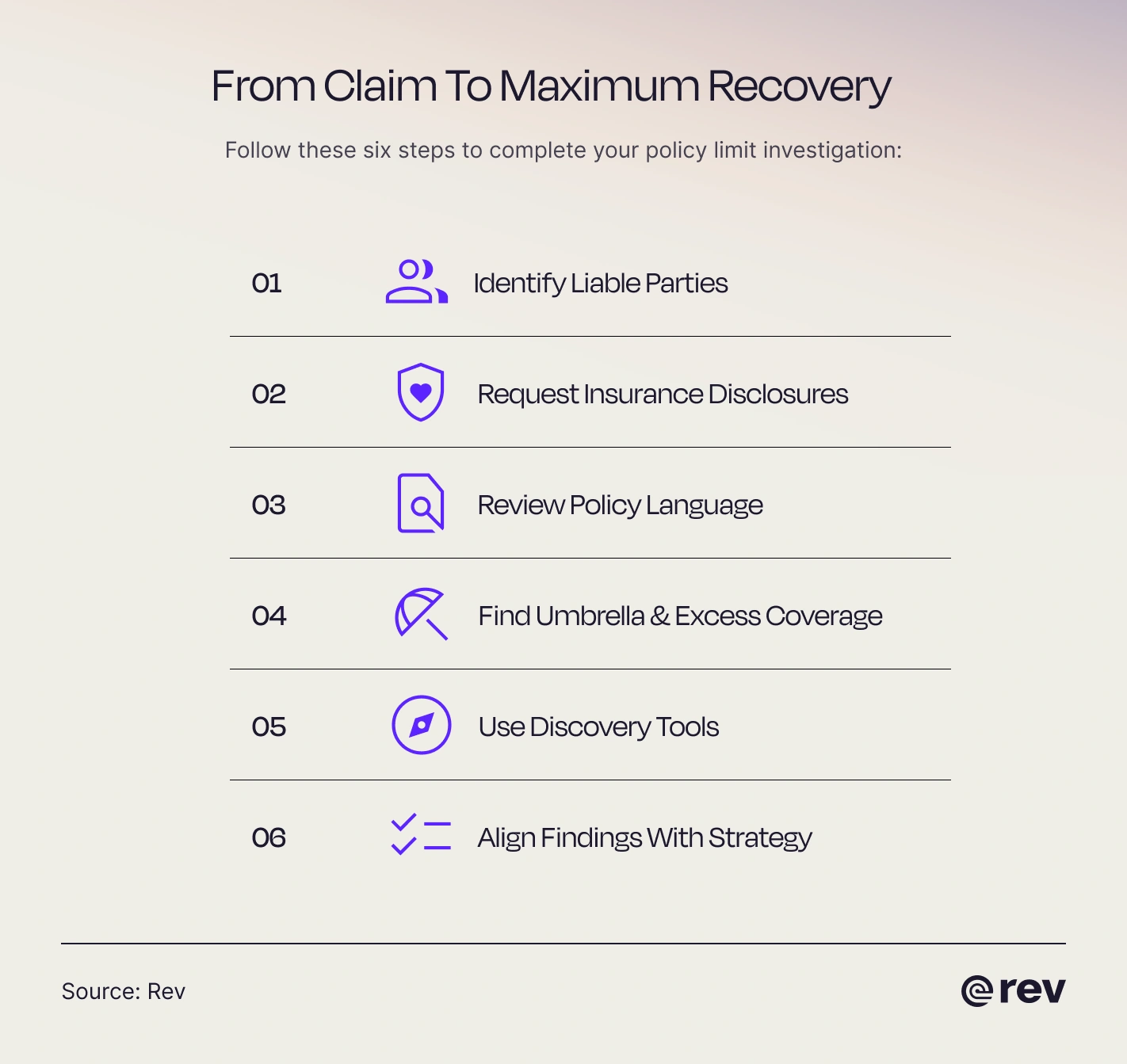

How to Conduct a Policy Limits Investigation (Step-by-Step)

Understanding policy limits should be a baseline target in most PI cases, but getting there is anything but simple. The following steps help you conduct a thorough investigation — and put you in a stronger position to pursue a full policy limits settlement when it makes sense.

1. Identify All Potentially Liable Parties Early

A thorough policy limit investigation starts with identifying everyone — not just the obvious defendant — who could potentially share liability. This begins at intake and continues through early case development, using sources such as police reports, incident reports, witness statements, and client interviews. Attorneys must dig beneath the surface to unearth relationships that might reveal additional coverage, whether that’s employer liability, property ownership, or contracted third parties.

The key thing to remember is that insurance coverage follows liability. Missing a party may mean overlooking an entire policy or multiple layers of coverage tied to that party. A driver acting within the scope of employment, for instance, may have commercial coverage with significantly higher limits than their personal policy.

Identifying these connections early will help you build the case around the full spectrum of potential recovery. And the earlier you map out all potentially liable parties, the easier it is to preserve evidence and request the right disclosures as the case progresses.

2. Request Insurance Disclosures And Policy Documents

With a full list of potentially liable parties in hand, the next step in your legal policy limits search is to formally request insurance information tied to each one. This typically starts with pre-suit demand letters and statutory disclosure requests (where applicable), asking for declaration pages, policy limits, and any applicable coverage positions.

These initial disclosures are important for establishing an early case strategy, including valuation and settlement posture. But they’re not always complete. Carriers may provide only partial information or delay responding altogether, which makes it critical to document requests and follow up consistently. In some jurisdictions, an insurance company’s failure to disclose can become a point of leverage later in the case.

As with every step in your policy limit research, timing is key. These requests should go out as early as possible to avoid delays and give you time to verify what’s missing.

3. Analyze Policy Language, Coverage, And Exclusions

This step (and the ones that follow) separates superficial investigations from comprehensive inquiries. The goal here is to carefully review the language by looking past the stated limits. Declarations pages provide a snapshot, but the full policy reveals what is actually covered and under what conditions.

A detailed search should seek to understand how coverage is structured (per person vs. per occurrence), identify any exclusions or endorsements, and note whether the insurer has issued a reservation of rights. Policy language may also open the door to additional coverage arguments that aren’t obvious from initial disclosures. At the very least, a clear understanding of coverage terms strengthens your position when anticipating insurer defenses and drafting demands.

4. Investigate Additional And Umbrella Coverage

Investigations should rarely stop at a personal policy disclosure — or even multiple third-party disclosures. There are often additional layers of coverage to explore, including umbrella or excess policies. Uncovering these may involve reviewing asset information, prior claims, corporate structures, or deposition testimony that points to higher-limit coverage.

Umbrella and excess policies often represent the largest source of recovery in serious injury cases. A case that initially appears capped at a standard auto or general liability limit may actually have significantly more coverage sitting above it. This extra coverage doesn’t always surface voluntarily, which means attorneys need to dig for the maximum amount deliberately.

5. Use Discovery To Compel Full Disclosure

When voluntary disclosures leave holes, legal teams must turn to formal discovery to capture complete policy information. Tools at this stage include interrogatories, requests for production, and depositions — particularly of corporate representatives or claims adjusters — focused specifically on insurance coverage and policy limits.

The advantage of discovery is that it allows attorneys to lock in answers under oath. That makes it a more legally forceful way to uncover inconsistencies, omissions, or previously undisclosed coverage. It’s also an opportunity to identify related documents, such as internal communications or prior claims, that may point to additional policies or higher limits.

6. Align Findings With Your Demand Strategy

Once you’ve verified all available coverage, it’s time to connect that coverage with the realities of the case — determining whether damages exceed policy limits, structuring a policy limits demand, and timing that demand to maximize leverage.

Organization is critical at this stage of prepping for a personal injury trial. Pulling together medical records, expert opinions, and key facts into a cohesive demand package requires quick access to accurate information. The stronger and more complete your investigation, the better you can position the case for maximum recovery.

Special Circumstances For Policy Limits

While most policy limit research follows the basic steps covered above, certain factors can add layers of complexity to the investigation. State law variations can be particularly important.

Florida law, for instance, requires insurers to disclose policy limits within 30 days of a written request. In Texas, meanwhile, insurers are not required to disclose limits pre-suit, so attorneys often obtain that information through the discovery process after litigation begins.

Cases involving multiple defendants or commercial policies are also more complex than single-party personal claims. Business-related claims often involve layers of coverage across entities, contracts, and insurers, making it more difficult to identify the full scope of available limits. Similarly, when multiple parties share liability, recovery may depend on how those policies interact.

Mass tort or multi-claim scenarios can be particularly time-sensitive. With aggregate limits shared across many different claimants, the pool of available coverage can shrink quickly. A late or poorly supported claim may significantly reduce what’s recoverable.

Strategies To Maximize Recovery

By now, you probably get the idea that timing and thoroughness are key to maximizing recovery.

As attorney Chaile Allen of The Law Firm of Chaile Allen notes, “Recovering the maximum available policy limits is much more likely when a case is thoroughly investigated as soon as it happens… Over time, critical evidence like security footage, physical evidence at a crash site, or data from a vehicle's computer could be lost.”

In other words, prompt, rigorous action preserves leverage. With that in mind, here are a few strategies to keep you from coming up short on potential recovery:

- Build your demand around documented leverage — not assumptions: The more complete and well-supported your demand package, the harder it is for insurers to justify delays or underpayment.

- Create pressure, not just a request: A demand is most effective when it introduces real risk for the insurer. Time-limited demands, supported by strong evidence, can force faster decisions, especially if exposure exceeds known policy limits.

- Anticipate coverage defenses early: Insurers will often look for ways to limit or deny payouts. If you can identify potential exclusions or gaps early, you’ll be in a better spot to counter those arguments before they weaken your claim.

- Use policy limits to shape negotiation strategy: Whether you’re pushing for a full limits demand or preparing for litigation, your strategy should reflect the ceiling of coverage and the strength of your case.

- Stay organized and connect the details. Key information is often buried in documents, depositions, and communications.

Common Misconceptions About Policy Limit Investigations

These types of liability limit investigations are so common in personal injury law that the nuances can be taken for granted. Several assumptions or misconceptions prevent attorneys from maximizing recovery for their clients:

- Misconception: The policy limits will be disclosed voluntarily.

- Reality: Initial disclosures are often incomplete or delayed. Attorneys should expect resistance and be prepared to pursue full policy information through follow-ups, policy limit research, and formal discovery.

- Misconception: There’s only one applicable policy.

- Reality: Many cases involve multiple layers of coverage — primary, umbrella, excess, or third-party policies. Stopping at the first disclosure can leave significant recovery on the table.

- Misconception: You can wait until later in the case to investigate.

- Reality: Early investigation is critical. Delays can weaken leverage and allow key evidence to disappear.

- Misconception: If the defendant has insurance, that’s enough.

- Reality: Coverage may be limited, disputed, or excluded. A thorough investigation is needed to confirm what’s actually collectible, not just what’s listed.

- Misconception: Policy limits don’t affect early case strategy.

- Reality: Limits often determine whether to pursue a case, how aggressively to litigate, and when to push for a settlement.

- Misconception: This is just paperwork.

- Reality: Effective policy limit investigations are active, ongoing processes involving document review, depositions, and strategic follow-up

-

AI: The Ultimate Research + Drafting Assistant

Policy limit investigations generate a lot of documents, recordings, and testimony, which have historically amounted to time-consuming review work. But AI tools have become a force multiplier, helping attorneys quickly search, organize, and extract key details from these materials.

Instead of manually combing through files, legal teams can surface mentions of insurance coverage, liability relationships, or prior statements in seconds. With the help of AI-powered tools like Rev, investigative transcripts become fully searchable and easy to navigate, so attorneys can quickly pinpoint key moments in audio or video recordings and pull exact language to support their case.

Technology can also accelerate the process of drafting case strategy or demand letters. As firms adopt more streamlined workflows, they can move faster without sacrificing accuracy, putting them in a stronger position to pursue maximum recovery.

Expand Your Limits With Rev

Personal injury claims are all about maximizing value for your clients, and it’s impossible to do that without a detailed investigative strategy. The more clearly you understand available coverage and insurance limits, the more effectively you can shape strategy, apply pressure, and pursue maximum recovery.

The right tools can make that process faster, more organized, and more precise. From uncovering key details in transcripts to building stronger demand packages, having instant access to critical information can transform your strategy — and case outcomes.